)

Sustainable business

28.05.2021

Carbon Accounting and Your Business Footprint

Our approach to business carbon accounting …

)

reporting on sustainability are now doing it across more than one framework simultaneously which can be time consuming (or similar). Today, businesses are expected to demonstrate the credibility of their carbon credit purchases, report on biodiversity impacts, assess nature-related risks, and provide evidence to support environmental claims.

At the same time, sustainability teams are navigating a growing number of reporting frameworks, each with its own requirements, metrics and terminology.

Earthly provides transparent, project-level environmental data that helps businesses meet disclosure requirements across leading sustainability frameworks. Rather than collecting different datasets for different standards, organisations can access one source of information designed to support multiple reporting needs.

Sustainability disclosures are becoming as important as stakeholder expectations.

Businesses must report not only on emissions, but also on credibility, biodiversity impacts and nature-related risks.

Leading frameworks such as SBTi, TNFD, IFRS, ESRS, SBTN, ISO 14068-1 and the GHG Protocol often require similar environmental data.

Multiple disclosure frameworks can create reporting challenges.

Earthly's Keystone 3.0 provides audit-ready project data.

Sustainability disclosure frameworks are structured standards that require or guide businesses to report on their environmental, social, and governance impacts in a consistent, verifiable way. They give investors, regulators, customers, and other stakeholders reliable information about how a business is managing its sustainability risks and commitments and to hold companies accountable for the claims they make.

For nature investments specifically, disclosure frameworks matter because they define exactly what data a business needs to hold, what it needs to report, and how that reporting will be scrutinised.

Buying a carbon credit or a biodiversity credit is only the beginning for climate action. The data behind that investment is what allows you to report with confidence, defend your claims, and demonstrate real impact to the stakeholders who matter.

According to EY's 2025 Nature Action Barometer, 93% of companies mention nature in their reporting, but only 26% can evidence that impact. Earthly helps bridge that gap by providing the transparent, project-level data businesses need to evidence the impact of their nature investments.

Jump to:

Science Based Targets initiative - Corporate Net-Zero Standard V2.0

IFRS Sustainability Disclosure Standards - S2 Climate-related disclosures

The

(SBTi) Corporate Net-Zero Standard is the world's first science-based framework for corporate net-zero target setting. Version 2.0, published in June 2026, requires companies to set targets, report progress annually, and demonstrate credible action across their value chains.

introduces the Ongoing Emissions Responsibility (OER) framework, which brings together beyond value chain mitigation, carbon removals, and neutralisation under one integrated structure.

Companies with science-based targets must now:

Disclose voluntary nature investments against SBTi's OER recognition tiers.

Demonstrate that investments meet the framework's Goals and Principles for high-integrity impact.

Provide impact and monitoring data at the project level.

V2.0 requires verified mitigation outcomes, project-level impact data, and annual progress reporting against OER recognition tiers.

Keystone 3.0 metrics map directly onto SBTi's BVCM disclosure template.

Earthly's beyond-carbon approach - covering biodiversity, water, livelihoods, and ecosystem integrity alongside carbon - allows companies to demonstrate full alignment with BVCM Goals and Principles.

The impact and monitoring data V2.0 requires is built into every Keystone 3.0 assessment, available at the point of investment, not sourced separately after purchase.

The

(TNFD) provides a global framework for companies and financial institutions to identify, assess, manage, and disclose their dependencies, impacts, risks, and opportunities related to nature.

The TNFD recommendations require companies to disclose their dependencies and impacts on nature through their investments. Specifically:

Report investment-level metrics for each climate and nature project.

Disclose how your investments affect ecosystems, biodiversity and natural capital.

Report against TNFD's core and additional disclosure metrics.

Support your disclosures with structured, evidence-based project data.

General statements about nature commitments will not satisfy a TNFD report. You need to report against TNFD's investment-level metrics (A21.0, A23.2, A24.0, A24.3, A24.4) and its full set of impact metrics for core and additional disclosure. If your provider does not structure that data, your team has to build it manually - typically from project PDFs that were never designed with TNFD in mind.

Earthly provides the relevant TNFD investment-level metrics (A21.0, A23.2, A24.0, A24.3, A24.4) for each investment as standard.

Keystone 3.0 maps directly to the full set of required TNFD impact metrics: C1.0, C1.1, C2.0, C7.3, A2.2, A3.1, A4.0, A5.1, A5.2, A5.3, A5.4, A6.0, A23.3, and A24.1

Structured, disclosure-ready data is available from the point of investment, eliminating the need to manually compile reporting information from project documents.

Project-level monitoring is one of the many data sources used to assess projects on the Earthly Marketplace, giving businesses the evidence needed to report confidently across leading sustainability disclosure frameworks.

sets out requirements for companies to disclose climate-related risks, opportunities, and the use of carbon credits. It is being adopted across more than 30 jurisdictions representing over 40% of global market capitalisation.

For nature investments, S2 focuses specifically on the credibility and integrity of carbon credits - what they are, who certified them, and whether they are genuinely additional and permanent.

IFRS S2 requires companies disclosing carbon credit use to demonstrate the credibility and integrity of those credits:

Evidence that credits are additional, permanent and managed for leakage risks.

The certification scheme under which the credits were issued.

Project-level information that supports transparent, decision-useful disclosures.

Vague references to "high-quality credits" will not satisfy an IFRS disclosure. You need a credibility analysis covering the dimensions IFRS considers material; and that documentation needs to exist at the point of purchase, not be assembled months later.

Keystone 3.0 provides a sector-leading credibility and integrity analysis across multiple dimensions, including permanence, for every credit in the Earthly portfolio.

At the point of purchase, buyers receive the number of credits, the certifying scheme, and the credit type.

Everything needed to support IFRS disclosures is included with your investment, helping streamline reporting and improve transparency.

The

(ESRS) strengthens the EU's Corporate Sustainability Reporting Directive (CSRD). ESRS E1-7 specifically covers carbon credits used toward climate targets, requiring companies to disclose the volume, standard, biogenic sink classification, and location of credits at the point of purchase.

It is mandatory for large EU companies and relevant for non-EU companies with EU operations, customers, or investors.

ESRS E1-7 requires companies to disclose the credibility and integrity of carbon credits used toward climate targets. Requirements include:

Credit volume, standard, biogenic sink classification, and location - all traceable to the point of purchase.

Multi-year and forward contracts reportable as planned cancellations.

Data structured to support that reporting approach from the start of the investment.

ESRS does not allow for retrospective data collection. The information has to be there when the investment is made, which means your provider's data infrastructure matters as much as the quality of the projects themselves.

Keystone 3.0 is structured to align with ESRS E1-7 disclosure requirements, helping streamline sustainability reporting.

Key credit information, including volume, standard, biogenic sink classification and location, is available at the point of purchase, making it easier to support ESRS disclosures.

Multi-year and forward contracts are structured to support reporting as planned cancellations, reducing manual work when preparing disclosures.

The

(SBTN)’s Science Based Targets for Nature extends the science-based targets approach beyond carbon to cover freshwater, land, ocean, climate, and biodiversity. It provides guidance for companies to set and disclose nature-related targets, requiring data on biodiversity credit purchases and investment amounts broken down by ecosystem and activity type, structured for attribution to specific SBTN categories.

What SBTN requires from your nature investments

SBTN disclosure requires:

Data on biodiversity credit purchases broken down by ecosystem and activity type

Impact metrics attributable to specific SBTN categories: freshwater, land, ocean, climate, and biodiversity

Investment data structured for attribution, not aggregated across projects

A lump-sum investment across multiple projects with no breakdown by ecosystem or impact type will not satisfy SBTN reporting. The data needs to be categorised from the point of investment, not reconstructed from project documents after the fact.

How Earthly helps you meet it

Investment data is broken down by ecosystem and activity type, making it easier to attribute nature investments accurately.

Keystone 3.0 reports impact metrics across all five SBTN categories-freshwater, land, ocean, climate and biodiversity.

Project data is already structured for attribution, reducing the manual work needed to prepare SBTN-aligned disclosures.

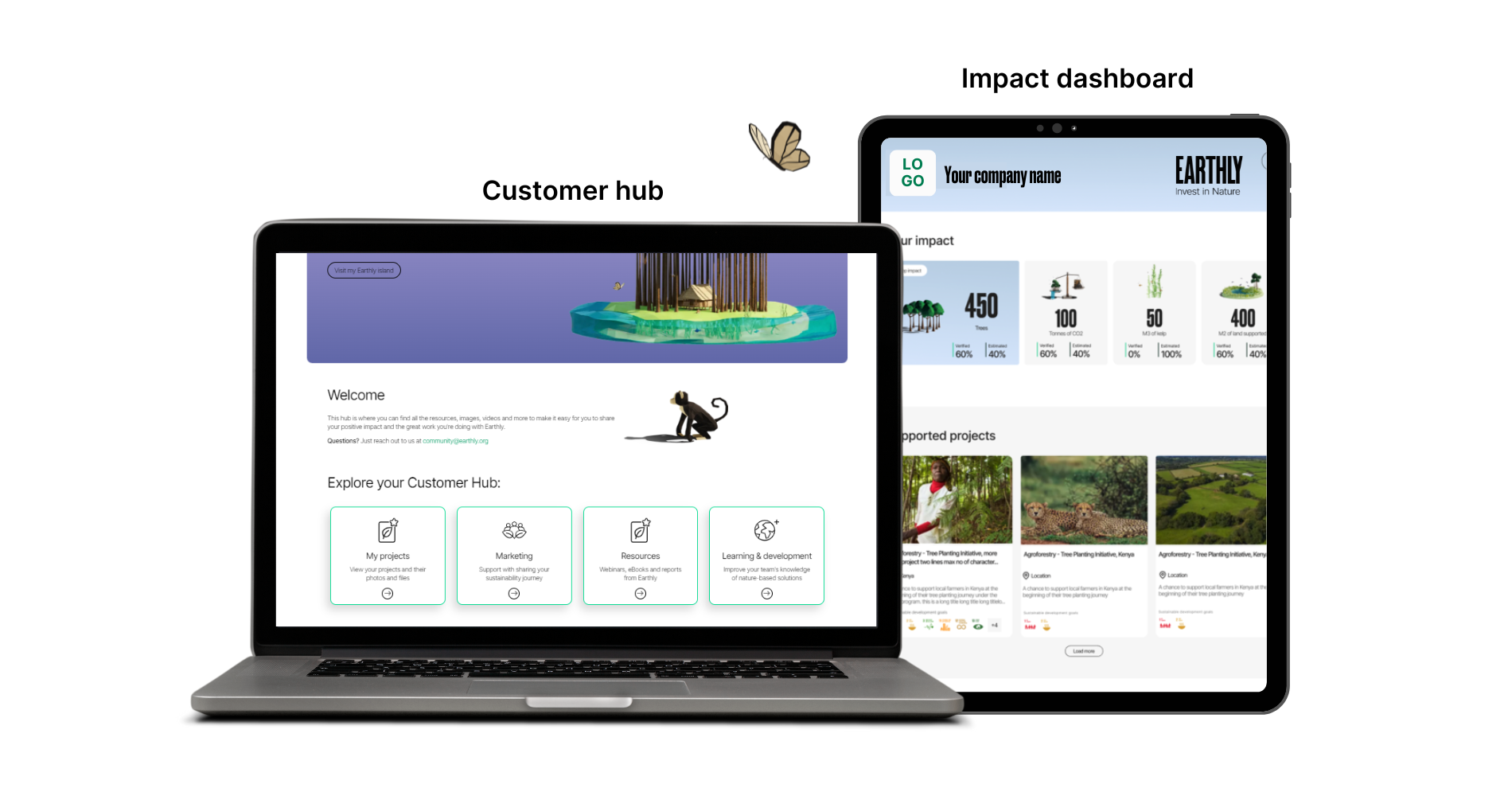

Earthly helps you go beyond sustainability reporting. Our Impact Dashboard and Customer Hub transform disclosure-ready data into clear, credible stories that you can confidently share with investors, customers and other stakeholders.

is the international standard for demonstrating carbon neutrality. It sets requirements for quantifying, reducing, and offsetting greenhouse gas emissions, and specifies what credit identification data companies must hold - including type, vintage, certifying body, and retirement record.

It also defines Core Principles for carbon credit quality that any portfolio used to support a carbon neutrality claim must meet.

ISO 14068-1 requires:

Detailed credit identification data: type, vintage, certifying body, and retirement record.

Alignment with ISO's Core Principles on carbon credit quality and integrity.

Documented evidence that exists before a carbon neutrality claim is made, not assembled under pressure if the claim is later challenged.

Keystone 3.0's carbon assessment aligns directly with ISO's Core Principles, helping you evaluate credit quality and integrity.

Every investment includes complete credit identification details, including credit type, vintage, certifying body and retirement record.

Earthly's portfolio is aligned with ISO's recommendations on credit type, vintage and quality, giving you the evidence needed to support credible carbon neutrality claims.

The

is the most widely used international accounting framework for quantifying and managing greenhouse gas emissions. Its accounting requirements form the foundation on which most other disclosure frameworks above are built. If the data does not hold up against the GHG Protocol, it will not hold up anywhere else.

The GHG Protocol's requirements on nature investments are specific and non-negotiable:

Baseline: what emissions would have occurred without the project?

Additionality: whether the project would have happened without carbon finance.

Leakage: whether emission reductions are displaced rather than genuine.

Permanence: whether sequestered carbon will remain stored.

Double counting: whether the same reduction is claimed by more than one party.

Every nature investment that feeds into your carbon accounts needs to be defensible against all five tests. If your provider cannot give you that data, your carbon accounting has a gap, and so does every disclosure framework built on top of it.

Keystone 3.0 carbon sections map directly to each GHG Protocol accounting issue: baseline, additionality, leakage, permanence, and double counting.

At the point of investment, Earthly provides all the data your team needs for GHG Protocol disclosure.

There is no gap between what you purchase and what you can evidence in your carbon accounts.

The

(CDP) is one of the world's most widely used environmental disclosure platforms, used by over 23,000 companies globally. It runs an annual questionnaire across three areas: climate change, forests, and water security.

CDP is primarily focused on value chain management rather than offsets, but nature investments, carbon credits, and biodiversity credits are directly relevant to several key questions in the questionnaire.

CDP's questionnaire includes several questions where nature investments, carbon credits, and biodiversity credits are directly relevant responses. The four most applicable are:

Question 3.1.1: Requires companies to detail environmental risks that have had or are anticipated to have a substantive effect on their organisation, with nature-based solutions, restoration, conservation, biodiversity offsetting, and voluntary engagement in conservation projects listed as recognised primary responses.

Question 3.5.4: Asks companies to describe their strategy for complying with environmental regulations, with the purchase of carbon credits listed as an eligible compliance strategy.

Question 4.5.1: Requires further detail on monetary incentives provided for the management of environmental issues, with restoration and compensation to address past deforestation and conversion included as a recognised performance metric.

Question 5.10.1: Asks companies to provide details of their internal price on carbon - relevant where nature investments form part of a company's internal carbon pricing strategy.

Earthly provides carbon and biodiversity credits directly relevant to CDP questions 3.1.1, 3.5.4, 4.5.1, and 5.10.1. Beyond credits, Earthly can also support the development of nature-based solutions within your value chain, which is relevant to the broader set of CDP questions focused on value chain management and environmental risk response.

Carbon and biodiversity credits purchased through Earthly provide verified, traceable evidence for CDP responses on environmental risk management and compliance strategy.

Keystone 3.0 data supports the level of detail CDP requires - covering project type, location, standard, and impact metrics

Earthly's nature-based solutions development capability means your CDP responses can go beyond credit disclosure to demonstrate active value chain engagement with nature.

Keystone 3.0 maps to major sustainability disclosure frameworks, giving you audit-ready nature investment data. Every project is assessed for maturity and evidence quality, so your disclosures are backed by demonstrated project performance and the strength of the evidence behind it.

is Earthly's proprietary nature project assessment framework - the methodology that sits behind every investment made through Earthly. It evaluates projects across three core pillars: carbon, biodiversity, and people, with water risks and ecosystem health assessed throughout.

Here is what that means for your disclosure:

Ecosystem-agnostic and registry-agnostic:

Results are fair and comparable across project types, standards, and markets, so your data holds up regardless of which frameworks you report against.

Every project is scored for both maturity and evidence quality:

Every project is assessed on both its performance and the strength of the evidence behind it, so you can distinguish verified impact from unsubstantiated claims.

Less than 10% of projects screened make it to our marketplace:

Every project has passed Earthly's rigorous integrity assessment, giving you confidence that you're investing in projects with credible, measurable outcomes.

Earthly's

turn the verified data that feeds your disclosure into something every stakeholder can engage with.

Personalised Impact Dashboard:

A live, public-facing view of your nature investment performance across carbon, biodiversity, and people - updated in line with your investments and shareable directly from your website, sustainability report, or social channels

Customer Hub:

A resource centre where your entire team can access project updates, communication templates, and guidance to accurately speak about your nature investments - including resources to help you stay on the right side of green claims requirements

Together, these tools help you turn complex sustainability data into clear, credible stories that resonate with every stakeholder.

According to

, 76% of executives cite data quality as their top ESG reporting challenge, and fewer than 30% of organisations feel confident in the accuracy of their ESG data. With Earthly, every investment comes with transparent, audit-ready data, helping you meet leading sustainability disclosure requirements while communicating your climate and nature impact with confidence.

Browse our

to find high-quality carbon and biodiversity projects, or

to find the right solution for your specific reporting requirements.

According to UNEP, nature-based solutions protect, restore and sustainably manage ecosystems while addressing climate, biodiversity and broader societal challenges. Every project in the Earthly portfolio is assessed across all three dimensions - carbon, biodiversity, and people - so your investment is working across the full scope of what a high-integrity NbS is designed to deliver.

Why are sustainability disclosures important?

Sustainability disclosures help businesses demonstrate accountability, build trust with investors and customers, comply with evolving regulations and communicate progress towards climate and nature goals. Transparent reporting also helps reduce the risk of

by ensuring environmental claims are backed by credible data.

What is the difference between sustainability reporting and sustainability disclosures?

Sustainability reporting is the broader process of collecting, managing and communicating sustainability information. Sustainability disclosures are the specific information organisations publish to meet the requirements of reporting frameworks, standards or regulations.

What disclosure frameworks apply to nature investments?

The frameworks most commonly relevant to corporate nature investments include SBTi, TNFD, IFRS S2, ESRS E1-7, SBTN, ISO 14068-1, the GHG Protocol, and CDP - though the specific frameworks that apply to your organisation will depend on your sector, jurisdiction, and the nature of your sustainability commitments.

The EU's Corporate Sustainability Due Diligence Directive (CSDDD) is also cited as a major disclosure burden for EU-facing businesses. Most companies with serious sustainability commitments are reporting against more than one framework simultaneously, and each has specific data requirements that your nature investment provider needs to be able to meet.

Can one nature investment satisfy multiple disclosure frameworks at once?

Yes, most sustainability disclosure frameworks require similar information - project integrity, environmental impacts and carbon credit quality. Credits purchased through Earthly come with Keystone 3.0 data designed to meet the requirements of all seven simultaneously, so your team is not maintaining separate data sets for each framework.

Related articles

28.05.2021

Our approach to business carbon accounting …

)

06.01.2021

Startups Magazine featured Earthly as a tech platform providing businesses with a new way to lead the …

)

23.11.2020

Fighting climate change is a pretty big challenge. And that’s why it needs collective action, not just from …